It’s funny how quickly the perception of what is important changes. Two months ago, this past week was marked in red on our calendar as the most important week of H1 2024: the FOMC, the potential first rate cut of a series of three, maybe four, and the new Fed twelve-month prediction for the rate trajectory.

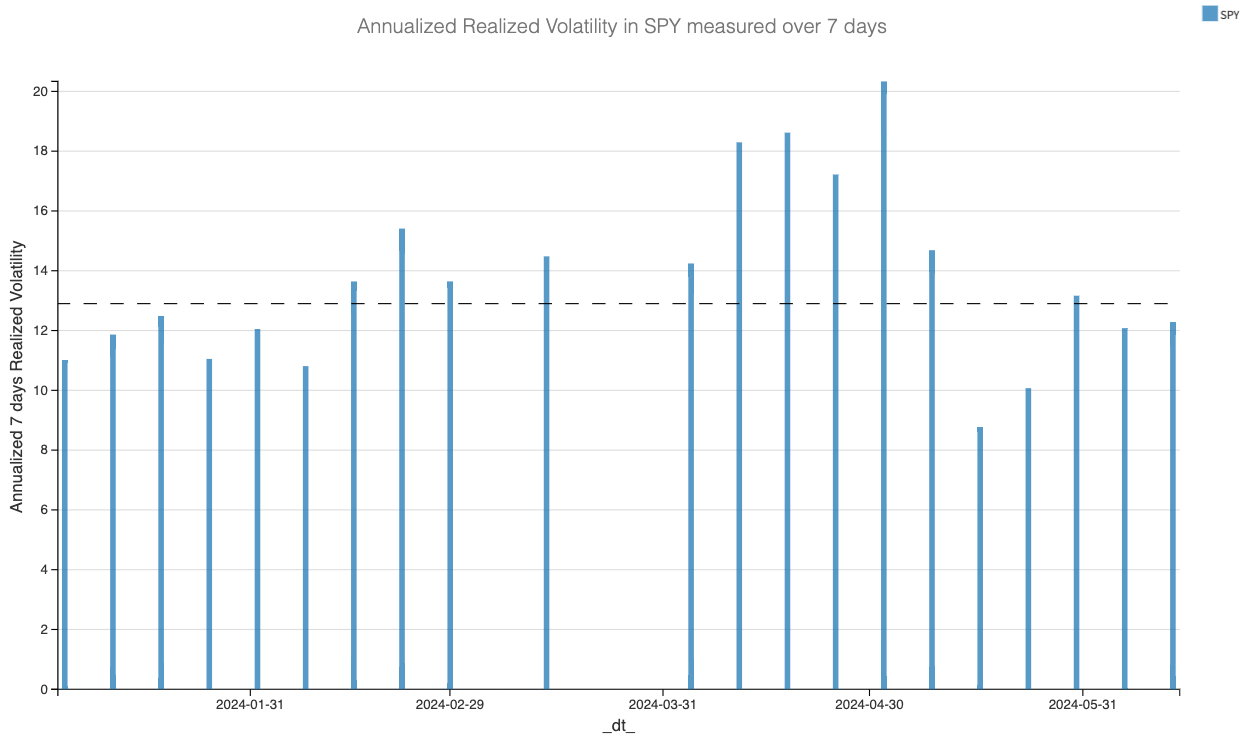

When all the dust settled, we couldn’t even reach the 50th percentile of the seven-day realized volatility measured on a Friday—in other words, for the week just ending.

Talk about a main event. In the end, the SP500 ended the week higher by 1.65% while the Nasdaq added 3.45%. The VIX didn’t even venture above 13.5 and closed Friday almost unchanged for the week at 12.66.

So, what happened? Well, pretty much what was expected and said over the past three months. Inflation came out slightly lower than expected on Wednesday morning, catapulting the market to a new all-time high. And if the Fed stayed as cautious as it’s been so far in 2024, preaching data dependency and carefulness not to break the relative success and stability currently observed in the economy, it still opened the door to a rate cut in September if inflation data didn’t go up again.

Far be it from us to criticize their modus operandi. Powell must have one of the trickiest jobs on Wall Street, and by many measures, he is doing a fantastic job.

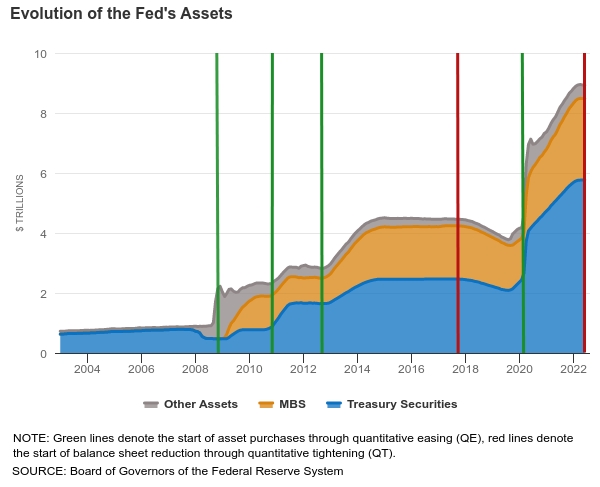

In trading terms, the Fed isn’t cornered and, in fact, is short theta in this occurrence—the more time passes without anything happening, the more the balance sheet is “coming back to normal,” and the amount of money in circulation is decreasing—at least in theory.

The Fed has a clear incentive to see the economy not falling apart and, as a consequence, the stock market not sliding dangerously to the downside, forcing them to expand their balance sheet again, which has a long way to go before normalization.

And what is the simplest way to be short theta and bullish? It’s to be short put, of course. Therefore, when buying puts at VIX 12, your counterparty, figuratively, is Jay Powell. Think about it: you are essentially betting he is wrong, big time, and so is the rest of the market.

Is this wise? Let’s look at Jay Powell's track record since his appointment as Chairman in February 2018.

The short side was a very difficult position to play, and being profitable requires a very specific set of skills reserved for only a select few—disproportionately present on social media.

Why have we put that chart up? To remind ourselves of two fundamental characteristics of the equity market:

- It tends to go up over a long period of time.

- It is quite noisy.

And next week may bring a little bit more noise in the market, and it may be tempting to lose sight of the big picture.

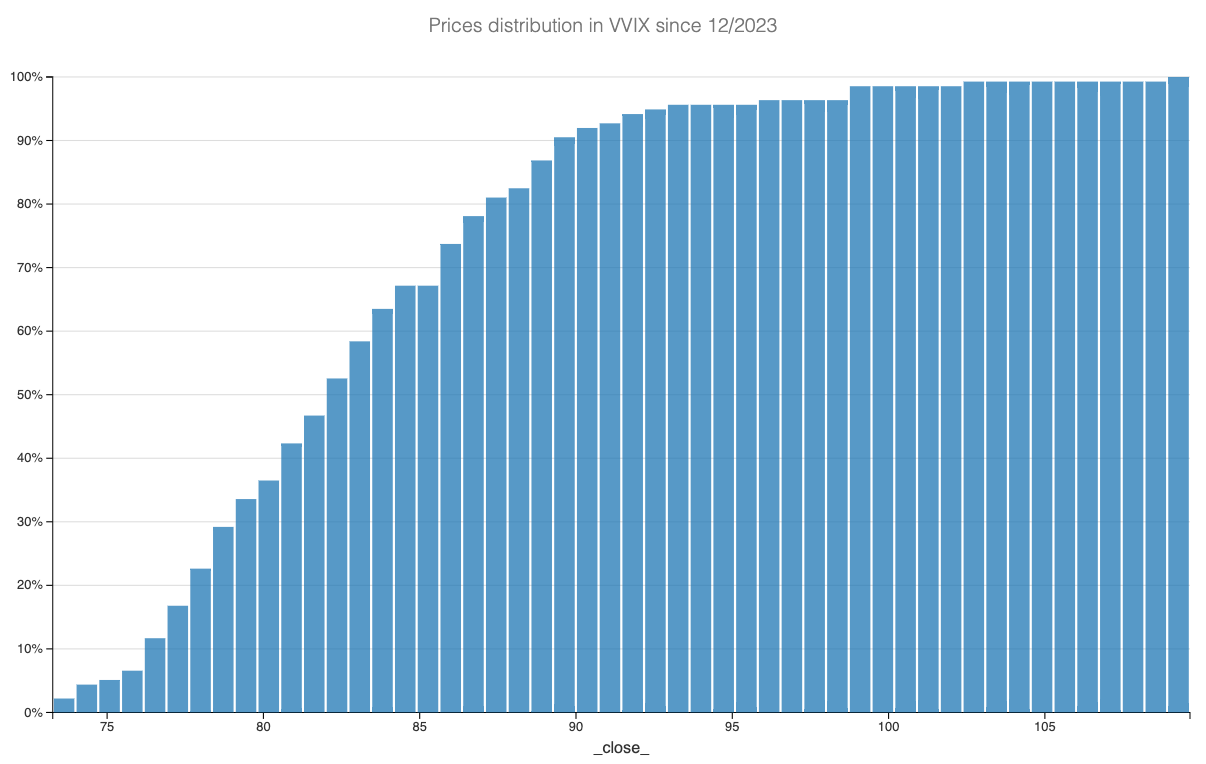

What makes us think that? VVIX. It closed at its highest in almost six weeks on no apparent news.

Two-thirds of the readings recorded in that super low regime were below 84. And although you should keep an eye on it, the current price actions may very well be driven by the mechanical effects of end-of-the-quarter rebalancing: some people leave their positions in June and purchase the following expirations.

That being said, we won’t read too much into this either—trying to find a directional advantage out of gamma is clearly out of our league and, once again, reserved for a select few. We will, however, stick to what’s been working really well so far in 2024: selling puts and buying cheap calls in risk reversals.

At the end of the day, this is what trading looks like—a lot of the same, with some small adjustments here and there based on market conditions. What do we need to see to change our view? A VIX meaningfully above 16 to start with and a new narrative in the marketplace. And remember the first chart in this article? A realized volatility over a week above 17, like the highs observed so far in 2024 during the tensions between Israel and Iran.

Sharpe Two is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

In other news

President Macron had to call for a snap election after the astonishing results from the far-right party in the European Election. The far-right movements are not a new thing in France or Europe. They’ve been brewing up over the years as the economic situation of many populations didn’t necessarily improve at the rate they were hoping, while some of the social constructs of European countries were heavily challenged by waves of immigration from the Middle East and Africa.

Nothing new here and so far the market has not felt bothered. But that may very well change if Le Pen is introduced as Prime Minister in early July. You may remember Greece, 13 years ago, crawling under debt and in a political chokehold? Their national debt was heavily sold by speculators, and the IMF had to negotiate a rescue package in exchange for austerity measures.We wish for Europe it won’t need one of its secular pillar to go under such a regime. However, sometimes, that is what it takes for the situation to improve: look at Greece right now, enjoying a Renouveau.

Thank you for staying with us until the end, and as usual, here are a few interesting reads from last week:

- It was Apple’s week last week when they announced a partnership with OpenAI. And while this took the spotlight, we realized we hadn’t heard about the Apple Vision Pro in a long time. Here is an excellent (and honest) review by .

- We stay in the world of AI with an interesting question from Jamin Ball for software vendors: is seat-based pricing dead ? Indeed, if most mundane tasks end up being replaced by AI, it poses an existential threat to many SaaS platforms.

That’s it for us this week. We wish you a pleasant week ahead. For our American readership, enjoy the holiday on Wednesday, and for the Europeans, enjoy the start of the Euro!

Ksander

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Have access to our indicators using our API.

Book a consultancy call to talk about the market with us.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.