Forward Note - 2024/02/16

A month later, and all time highs.

There we go! We've hit an all-time high again. After a month of sharp downside gaps driven by unsettling geopolitical news and shifting AI narratives, the market seems to have found its footing and decided—once again—that there’s not much to worry about.

The S&P 500 ended the week in the green, reaching fresh all-time highs, while the VIX closed in the 14 handle ahead of the long holiday weekend.

Had you asked us on Wednesday morning, this outcome wouldn’t have been on our bingo card. A hot inflation print initially rattled the market before the open, pushing it down nearly 1%, exacerbated by Powell’s comments earlier in the week reiterating—once again—that the Fed is in no rush to cut rates.

Yet, once the news was digested, a steady flow of buying orders and declining volatility carried stocks gently back to all-time highs—a level where they barely moved on Friday, one of the calmest sessions in the past two months.

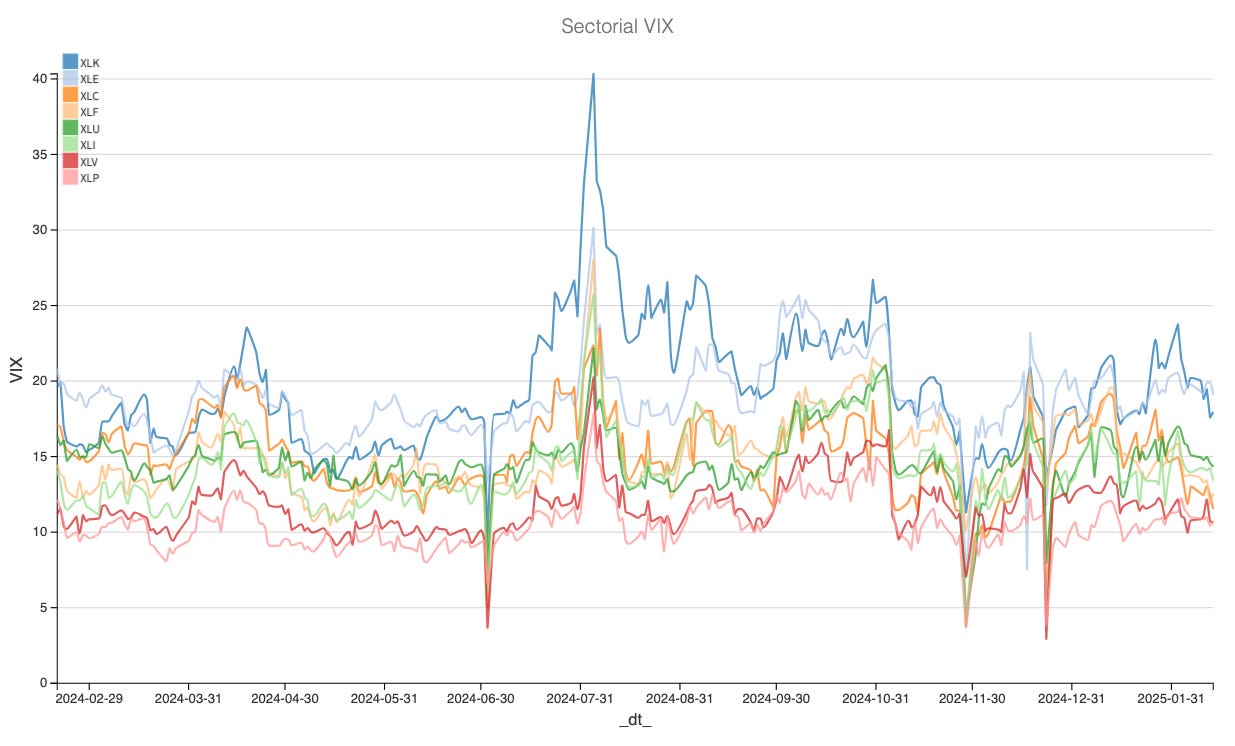

At this stage, it would be easy to call complacency and argue that the next bad headline could send markets tumbling. But this is where it pays to take a step back and reassess the thesis. First of all, an analysis of the VIX for the different sectorial ETF doesn’t scream concern, in particular in XLF, usually annunciator of turbulence ahead.

The market is well aware of the risks though. While we may be hovering near record highs, VVIX closed at 96.5 on Friday and though low compared to the past six months, is still on the higher end of its broader distribution.

In other words, the market sees a sharp VIX spike as more likely than a full-blown S&P crash. That distinction doesn’t negate the bigger picture, but it’s a reason to stay cautious—and, at the very least, to keep buying hedges.

But setting that aside, it’s hard not to admire the market’s ability to shrug things off and keep pushing forward. DeepSeek and the AI narrative getting overinflated? Fine, we’re still buying. Tariffs? What else you got. Inflation creeping back up? Call us when it’s flashing red.

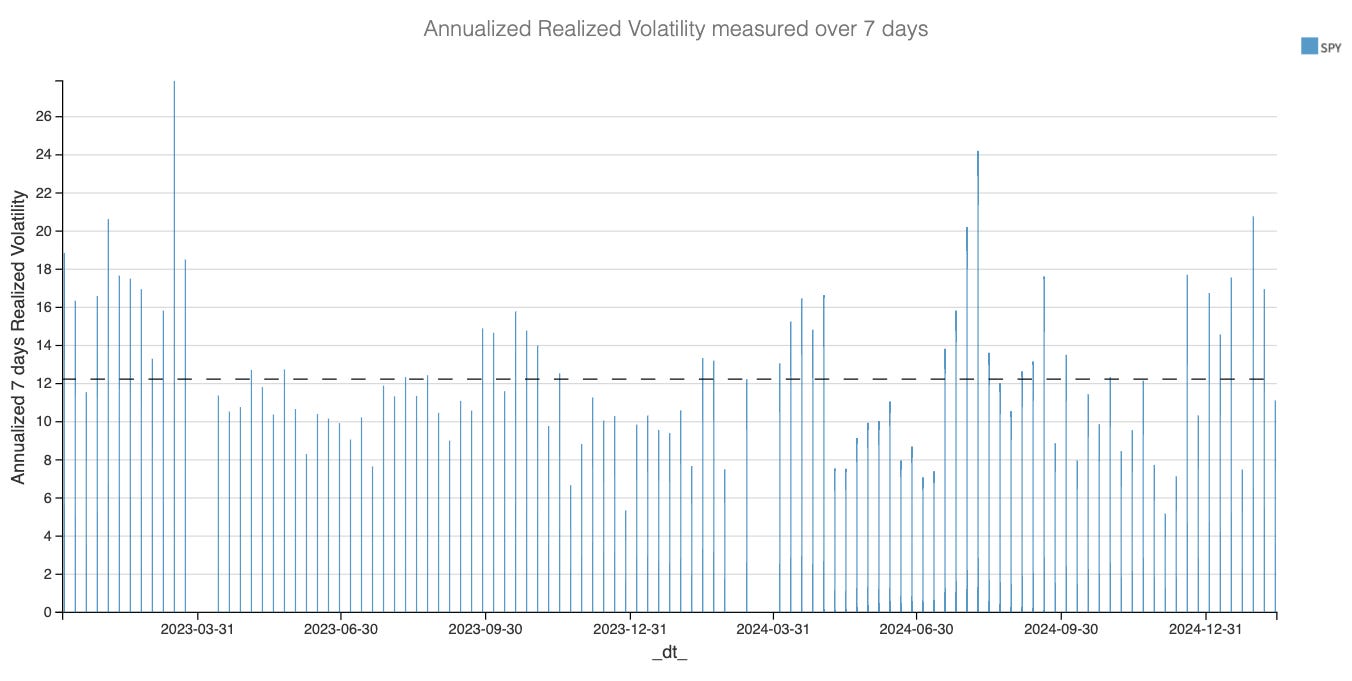

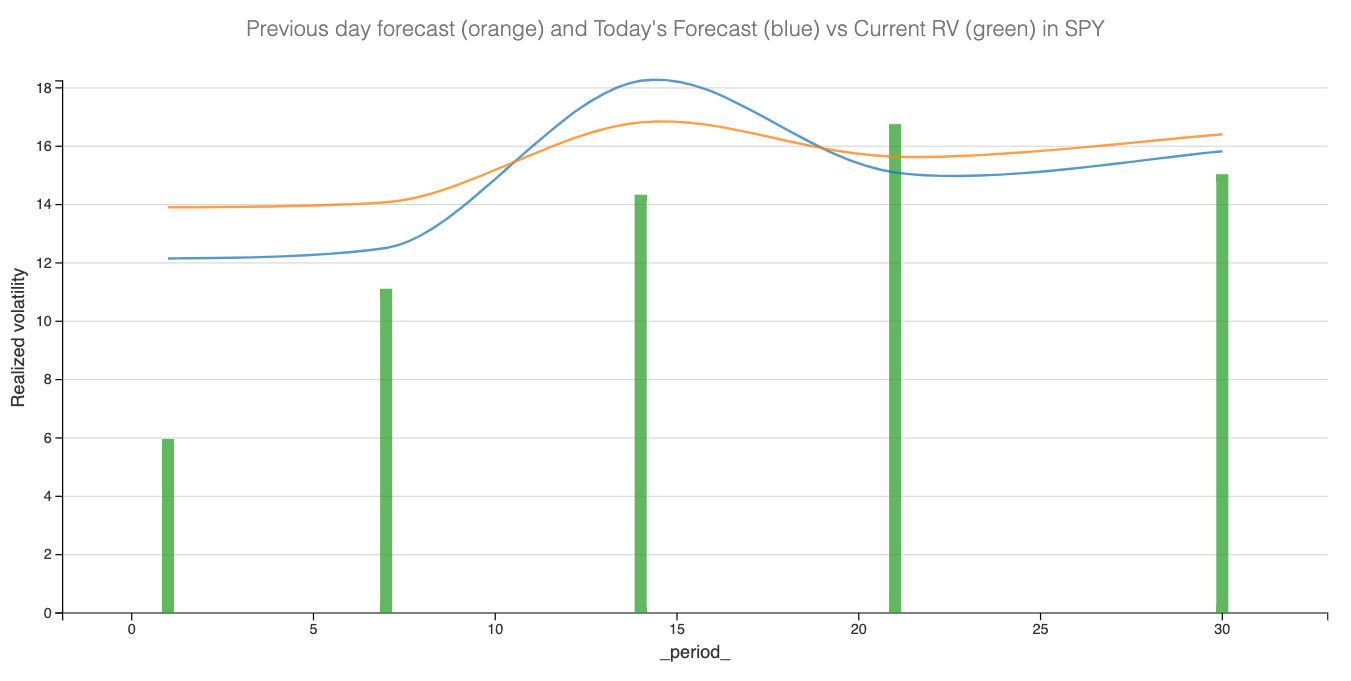

That’s not to say the backdrop isn’t turbulent—quite the opposite. Retail sales plunged in January, and the trade war looks more like it’s ramping up than easing, adding further inflationary pressure. Yet, for now, the market has adopted a wait-and-see stance, and that’s something we have to factor in: realized volatility forecast are steadily coming off what we were predicting a few weeks back, as the realized volatility at 30 days is now off the 16.5 mark.

In this environment, sticking too rigidly to a heavily short thesis could prove costly given the market’s resilience. And as we noted last week, index calls looked cheap. While they’ve gotten a bit pricier this week with the VRP finally making a comeback, they’re still not something we’re in a rush to get rid of.

As for puts—we remain torn. With VIX closing at 14.5 and despite realized volatility continuing to crumble, we’re still staying away for now.

The VRP is still clearly depressed in the back month and while you could make a case that the front weeks should work, we will focusing on areas of the market where it’s easier and more forgiving to sell volatiliy.

Feel free to laugh at our expense if you’ve been short puts over the past five weeks. The beauty (and frustration) of volatility trading is that you can’t entirely ignore the directional component of an option. While there may have been a few cold sweats along the way, selling puts was ultimately a bet on market resilience—and it paid off handsomely.

What’s next then?

As far as we’re concerned, the approach remains largely the same—we’ll continue hunting for opportunities where the market is overpaying. Right now, the best deals are still on the call side of VIX. Of course, this position carries risk, and we strongly advise caution with sizing. If possible, hedge by buying… well, the puts, which remain relatively cheap. Once again, if you believe a VIX spike can happen without a meaningful SPX move to the downside, feel free to ignore our thinking process.

Next week is a shorter one, with the U.S. markets closed Monday for Washington’s birthday. The calendar isn’t particularly intense—some PMI releases and a few Trump appearances, nothing the market hasn’t already adjusted to.

Then, it will already be time to shift focus toward NVDA earnings. While it might be early to expect DeepSeek to show up in their numbers, it will be fascinating to see how the market reacts—offering another key data point to refine the pricing of the AI thesis.

In other news

On Tuesday, we learned that Russia has agreed to release an American teacher detained for illegal possession and trafficking of marijuana—a supposed goodwill gesture in negotiations over Ukraine. Meanwhile, European diplomats are growing increasingly frustrated with the opacity of their American counterparts regarding their endgame for the conflict. Even more concerning, the U.S. seems in no rush to involve them more deeply in the peace talks.

If Putin and Trump had a lengthy discussion before Trump even spoke with Zelensky, no European leader was granted the same courtesy. Instead, they received a stern lecture from JD Vance about the dangers of democracy from within. While the Romanian case had us raising a few eyebrows a few weeks back, being schooled on democracy by a country that… well, where should we even begin? That, however, is beyond the scope of this newsletter.

Let’s stay calm and collected—just like the markets. The prospect of peace in Europe hasn’t gone unnoticed, and European stocks are off to a strong start this year, significantly outperforming their U.S. counterparts. If President Chirac were a trader, he might have summed up JD Vance’s remarks with a classic: Ça m’en touche une sans faire bouger l’autre.

(The translation is also beyond the scope of this newsletter)

Thank you for staying with us until the end. As always, here are a couple of good reads from last week:

While the world scrambles to pay tribute—one way or another—to what increasingly resembles Imperator Trump, hoping to avoid unnecessary punishment as global trade rules are rewritten, former ECB President Mario Draghi penned an interesting piece urging Europe to get its own house in order before fixating on the long-term damage of tariffs. Hard to disagree.

And because a feel-good story never hurt anyone, this week we came across the tale of Isaiah baker , who left Goldman to become a parking lot striper. No, this isn’t a call to quit your job on Tuesday morning, but reassessing priorities? That’s always a responsibility.

That’s it for us this week. Wishing you a great week ahead and happy trading!

Ksander

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.