It was another volatile yet convincing week for the equity market. The main indices were down more than 3% at some point, yet the S&P 500 closed up 0.6%, while the Nasdaq added another 1%. The VIX got crushed, closing below 14, and the market concluded on a very positive note after two dense weeks on the earnings and macroeconomic front.

The main event this week was the FOMC press conference on Wednesday. As expected, the committee kept interest rates unchanged but cooled off the pace at which it will reduce its balance sheet—a dovish sign that already set the tone for the press conference.

At first, Jay Powell didn't deviate much from the communication strategy initiated in the weeks before the event: the Fed will remain data-dependent in assessing when to cut rates, more likely later this year, as inflation remains stubbornly high.

However, pressed by journalists during the Q&A session, he admitted that a slowdown in the economy and, more importantly, a cooldown in the job market could also lead the Fed to cut interest rates this year.

Very conveniently, this Friday marked the first major miss in the NFP headline in over 18 months. Guess what the market reaction was? Extremely positive, indeed, well helped by yet another buyback program announced by AAPL during their earnings and a weaker ISM Services PMI, giving more credibility to the thesis of a cooling economy.

Another interesting point giving substance to a potential global slowdown is the heavy commodity sell-off. Prices are in free fall, and many economists see that as the first sign of deflation for an economy losing steam and momentum at an unprecedented pace.

You didn't need much more than that to revive the cynical commentaries describing how market participants were oblivious to risks and propelling prices while the economy was silently crashing.

If you've been a reader of Sharpe Two for a while, you know we refrain from making directional bets.

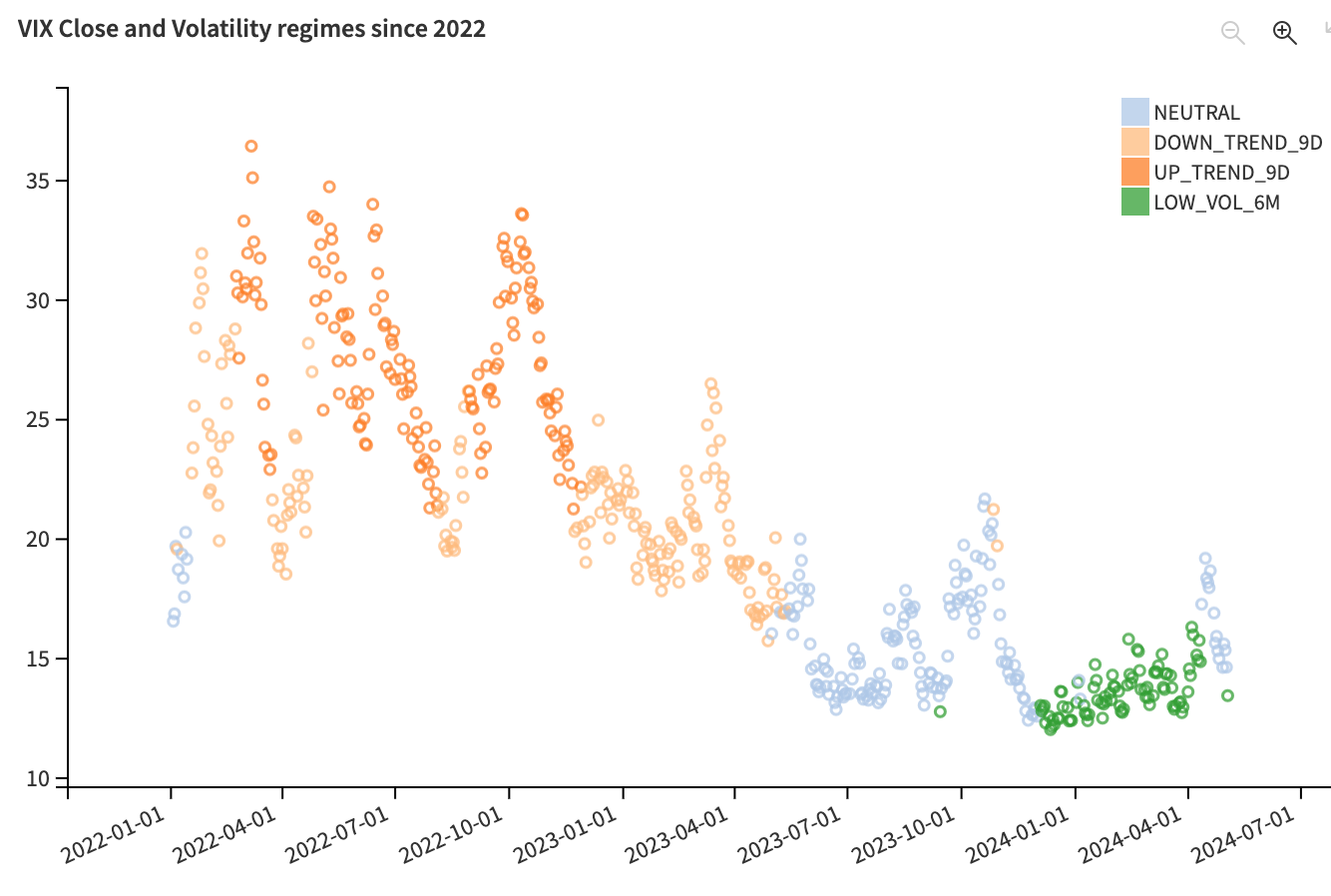

Instead, we refer to implied volatility as a forward-looking indicator of market expectations—a betting line, if you prefer. Our regimes detect that we are now back in a low-volatility regime, much faster than we would have anticipated.

Therefore, at VIX 14, the market is certainly not expecting a major recession within the next six months. A cooldown pushing the Fed to loosen up its monetary policies, yes, but nothing more.

Once again, we know that retail investors prefer the short side. We get it; it's more exciting and feels like being the main character in the video game "Me vs. Them." But remember that on the other side of your trade are fund managers with billions to invest, and they won't stay on the sidelines because the ISM is now showing a contraction, and the growth in Q1 was only 1.6%.

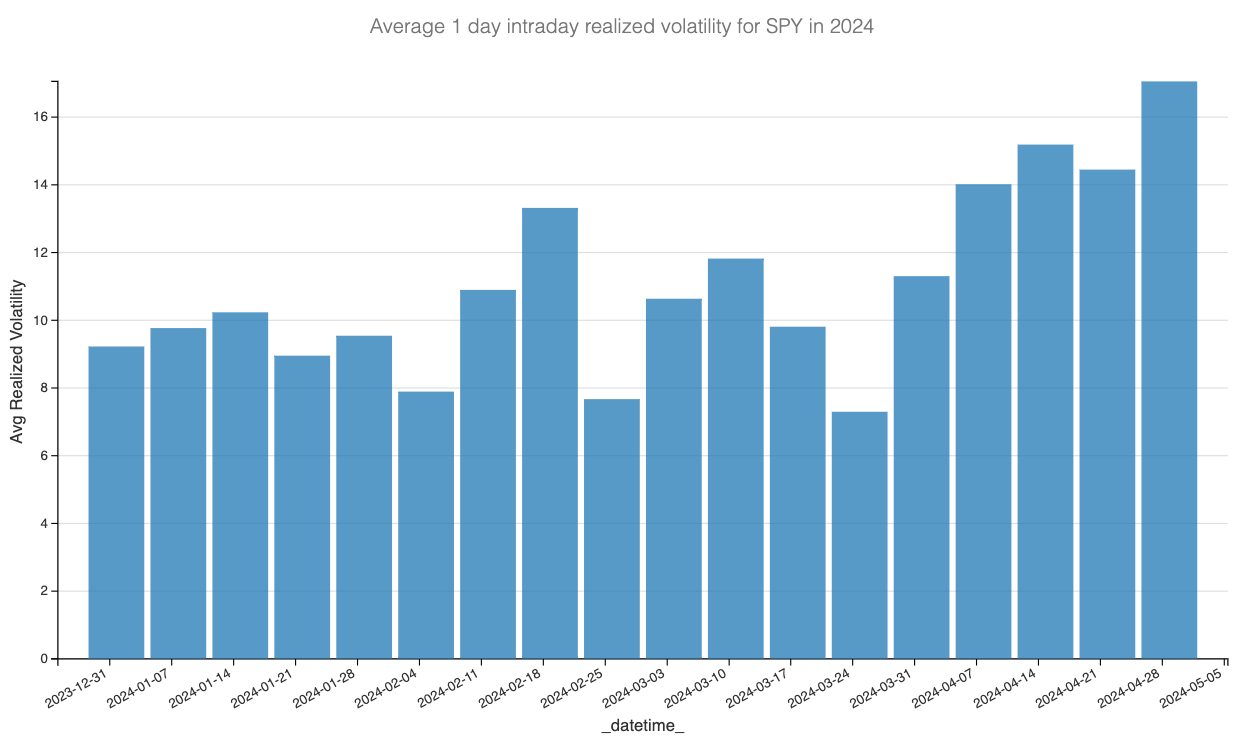

Talking about excitement, the intraday realized volatility was at the highest we've observed this year. Some peculiar movements were attributed to end-of-month flows at the close on Tuesday, followed by a beautiful reversal on Wednesday once the FOMC press conference was over, and more back-and-forth on Thursday; this was a scalper's dream and a bit of a nightmare for those collecting premiums.

That said, we will conclude by opening … an open door: realized volatility also means reversion. And with the next significant market event on the calendar being some inflation numbers (do they matter much now?) in 10 days and then the earnings from NVDA on May 22nd, our money is not on the scalpers but on the careful premium collectors.

But can you collect premiums at VIX 14? It's not because prices are low that margins have disappeared. In that sense, low-volatility sellers and Dollar Tree are not too different.

Sharpe Two is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

In other news

Market commentators love to corner the Fed, and the Fed always finds a way to uncorner itself. It's like watching a remake of the Tom and Jerry cartoon for adult children.

But what would we say about the BoJ? Despite their efforts to intervene and support the yen, the currency continues to weaken and hit new lows against other major currencies. The market constantly overpowers the BoJ's attempts to control the situation, leading to a loss of credibility for the central bank.

We thought hard about another cartoon analogy and came up with "They are big, and I am small, and that's not fair, oh no!" This catchphrase is from Calimero, the Italian cartoon character depicting a small black baby chick who wears half his eggshell on his head.

Just like Calimero, who never lets his size or the perceived unfairness of his situation stop him from striving forward, the BoJ may yet find a way to adapt its strategies and reassert its influence on the market. While the road ahead may be difficult, there's always the potential for a comeback story in the ever-shifting landscape of global economics. What if it would come from a slowdown in the US economy?

Thank you for staying with us until the end. As usual, here is a list of articles we found captivating this week.

- I worked in software sales for several years in various hybrid roles between tech and customer-facing positions. So when this article from about making it as an enterprise salesperson came out, I was amused and intrigued. The field is so diverse that finding a one-size-fits-all solution is hard. But this article is a good place to start for anyone who wants to understand more about the myth behind the title.

- Are you also tired of this endless debate about inflation? We are. In this article, makes a case for a new floor at 3%. We tend to agree with the narrative and wish it would become the new consensus so the market conversation can move on to more interesting topics.

- This week in Sharpe Two, we answered your most recurring question about our approach to volatility trading. Thank you again for all the positive feedback!

That is it for us this week; as usual, we wish you a great week ahead and happy trading!

Ksander

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Have access to our indicators using our API.

Book a consultancy call to talk about the market with us.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.