At Sharpe Two, our strategy is to identify opportunities in the volatility space that demand minimal intervention. We dedicate our efforts to scouting situations where the premium investors pay notably exceeds the actual movement in the underlying asset.

However, basing decisions purely on data can be a precarious approach. It's essential to have a fundamental rationale for each trade, explaining why the market consistently overpays for certain assets.

Contrary to popular belief among retail traders, the real drivers of market positioning and flow aren't just mathematical models or algorithms but rather the inherent flaws of the human psyche. These human elements influence fund managers' decisions, sometimes leading to seemingly irrational actions that disrupt the efficient market hypothesis.

Yet, upon closer examination, these 'irrationalities' can often be rationalized. When carefully analyzed, many of these market behaviors align with a utility function concept: the idea that investors are willing to pay a premium for assets they believe will be highly beneficial in the future.

Let's consider a concrete example to illustrate this concept further. Think about your approach to insurance: which do you tend to negotiate more aggressively for — car insurance or home insurance?

Unless you're exceptionally rational in every decision, you're likely to seek the cheapest option for car insurance while being more willing to pay a higher premium for comprehensive home insurance.

Why is this the case? Simply put, your home generally holds more value to you than your car. In the event of a catastrophe, you can find alternatives to a car, but losing your home is far more disruptive. You want the assurance that any damages to your home will be covered comprehensively and promptly, allowing you to return to normal life with minimal disruption. This example shows how perceived utility influences our decisions and willingness to pay a premium for certain assurances.

Understanding the role you play as an option seller in the marketplace is crucial to your profitability. When the market experiences a sharp movement, either upward or downward, it's often the option sellers who are called upon to 'foot the bill.' Your task, then, is to pinpoint where the market is most likely to overpay and to measure this potential with precision.

In today's analysis, we turn our focus to an emerging market ETF that has shown robust performance over the past six months. With careful sizing, this trade offers a valuable opportunity to collect premium fees while operating on a relatively automated basis.

Let's dive into the details.

The Context and the Data

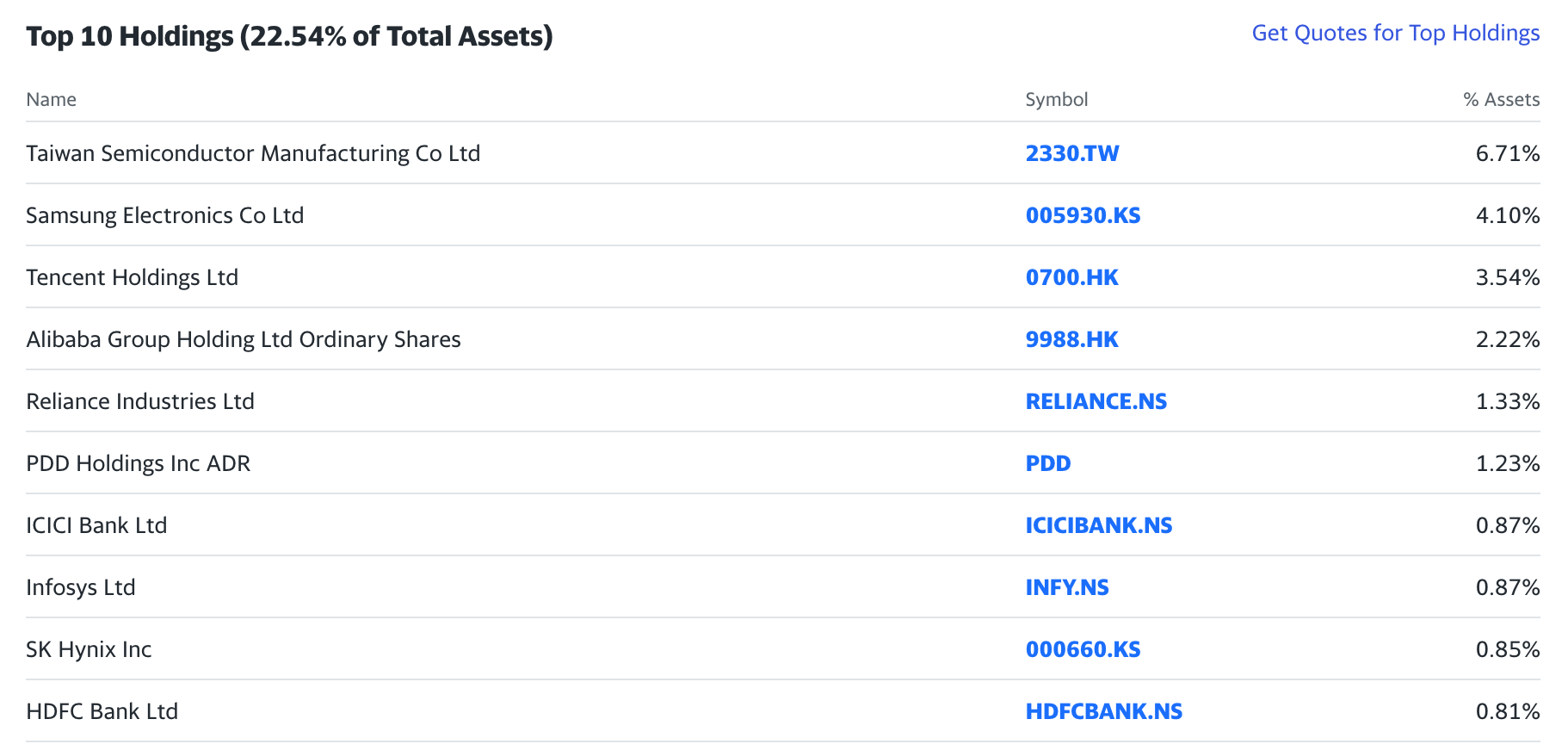

EEM tracks a range of companies in the emerging market space, though a closer inspection reveals that it's heavily invested in some of the largest names in tech and finance within Taiwan, Korea, and China.

While the top four holdings might be familiar to many, the remaining six, though perhaps less known globally, are formidable players in their own right. From my experience living in Asia and consulting in AI/data analytics for these companies, I can vouch for their significant market presence, rivaling our Western giants in many respects.

Having nearly 25% of the ETF invested in such quality stocks is a positive indicator. It suggests that the fund's managers are exercising due diligence, and in the event of a market downturn, the fund is well-positioned to maintain its stability.

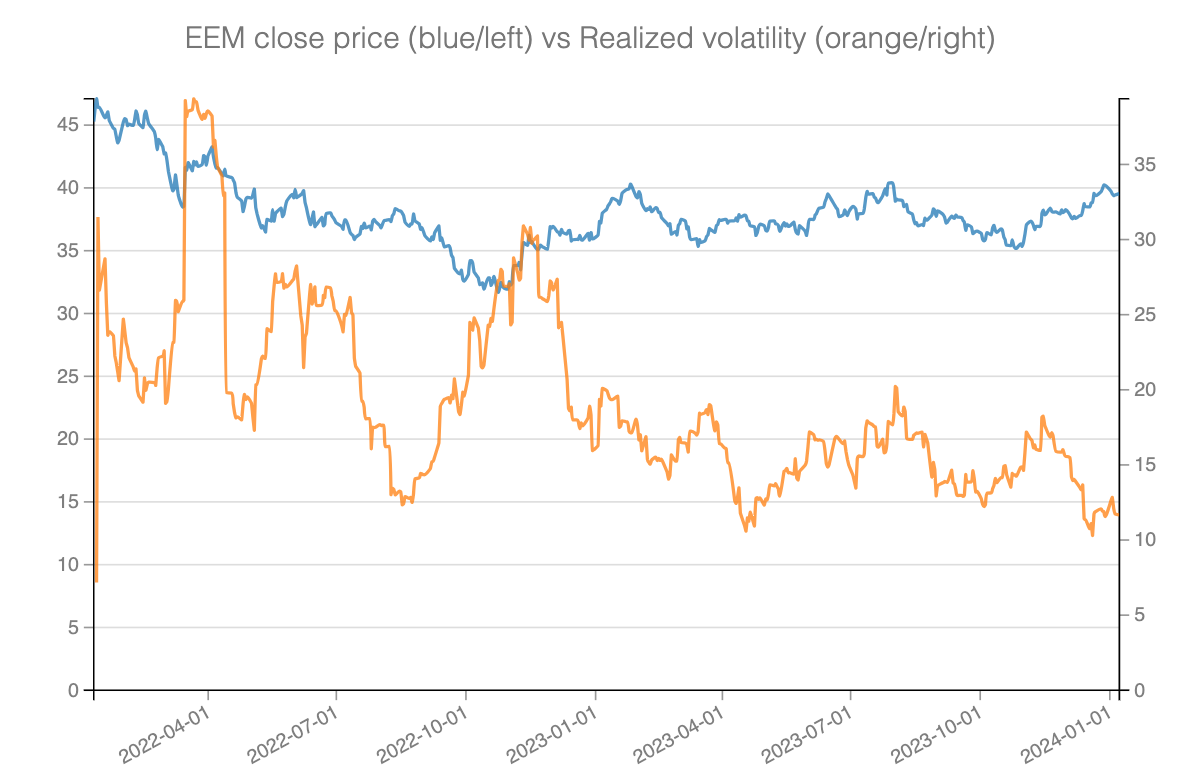

Indeed, the fund's performance over the past two challenging years not only supports this view but even surpasses expectations.

Despite its exposure to the often-volatile Emerging Markets sector, EEM demonstrated remarkable stability throughout 2023, consistently trading within the range of 30 to 35.

However, what stands out even more is the fund's realized volatility, which remained well-contained between 10 and 20 percent.

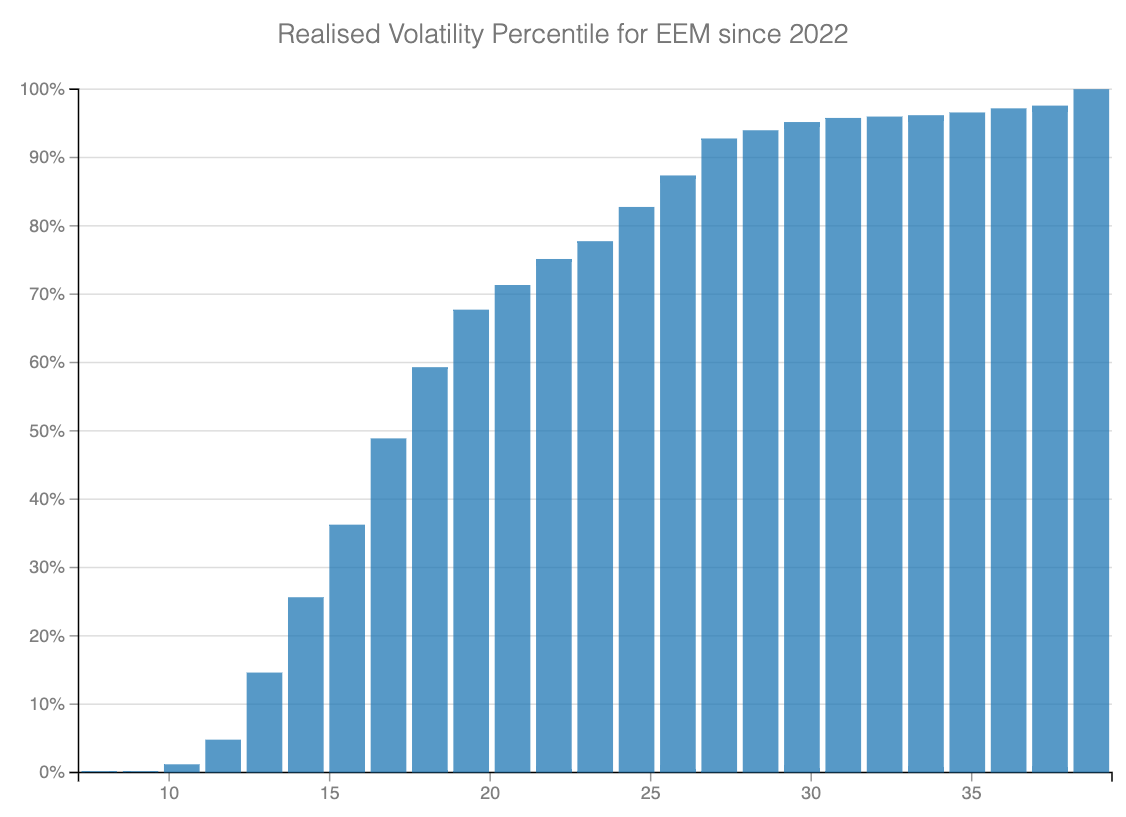

With the current realized volatility at 11.7%, EEM is positioned in the 13th percentile of its historical volatility range.

This observation serves as yet another example of the Variance Risk Premium at play. This premium — the difference between the price of At-The-Money (ATM) options and the actual movement realized in the underlying asset — tends to be at its highest when volatility is at its lowest.

This scenario exemplifies a type of market irrationality that actually makes a great deal of sense.

Traders, market makers, and fund managers concur that, despite EEM's effective management and signs of global economic improvement, emerging markets remain susceptible to volatility-triggering events. A potential economic slowdown or major geopolitical incidents, like the ones we've recently witnessed, could swiftly upset the balance. For example, we observed a notable spike in realized volatility in April 2022, coinciding with the onset of the Ukraine war.

This general consensus among market participants is mirrored in the inflated pricing of At-The-Money (ATM) options, which remains high despite the underlying stability of the fund.

As a result, even if realized volatility continues to decrease, the market is not likely to adjust its risk perception in tandem. This divergence leads to an ever-widening Variance Risk Premium (VRP).

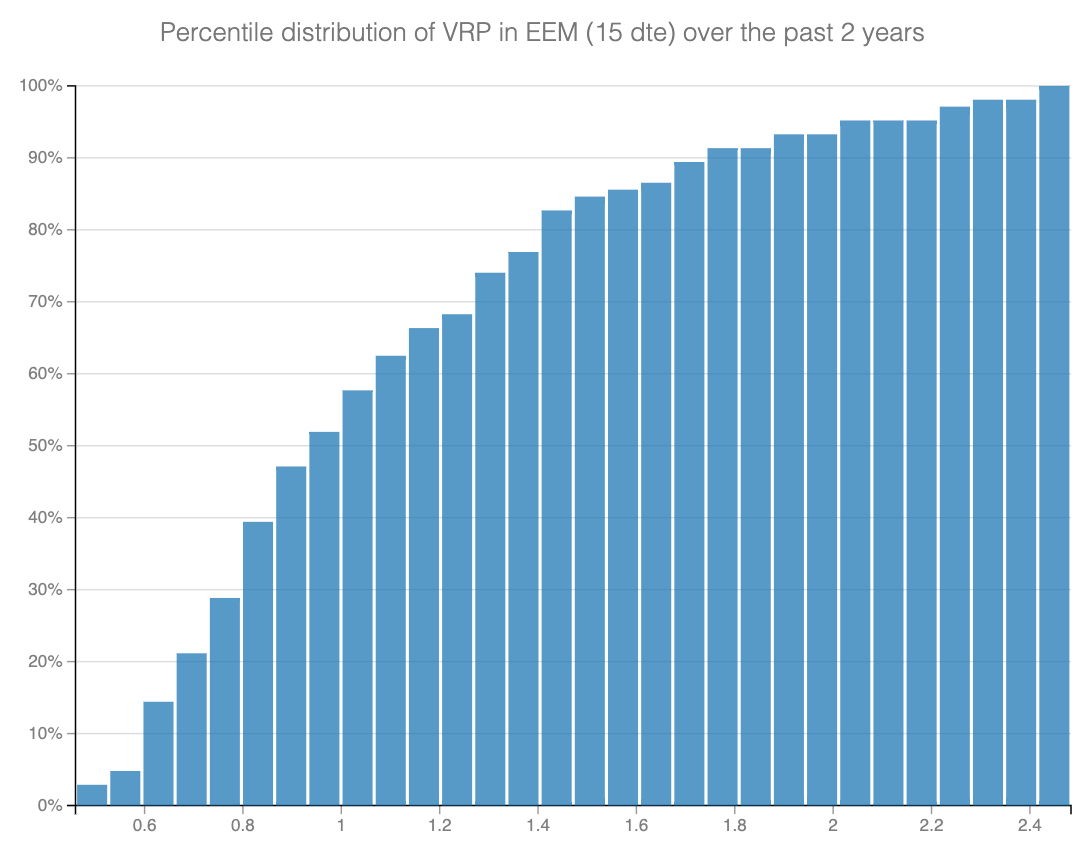

The current VRP, standing at 1.28, is positioned in the 75th percentile of its distribution over the last two years, underscoring the increasing gap between market expectations and actual volatility.

The Risks and the Performance

We understand the reservations of our more cautious readers – given volatility's mean-reverting nature, wouldn't now be the time to go long on volatility in EEM instead of short?

These are indeed valid concerns. Let’s first outline our proposed trade methodology and then delve into assessing its risk and performance.